Credit Card vs Debit Card – Key Differences Explained for Beginners, Full details 2025 updated

Credit Card vs Debit Card – Key Differences Explained for Beginners, Full details 2025 updated.

Difference Between Credit Card vs Debit Card Explained

In today’s digital age, plastic money is more common than physical cash. Two of the most widely used financial tools are credit cards and debit cards. While they may look similar and are used for similar purposes like shopping, paying bills, or online transactions, they function very differently.

Let’s break down the difference between a credit card and a debit card, their benefits, drawbacks, and how to decide which one is right for you.

Table of Contents

What is a Debit Card?

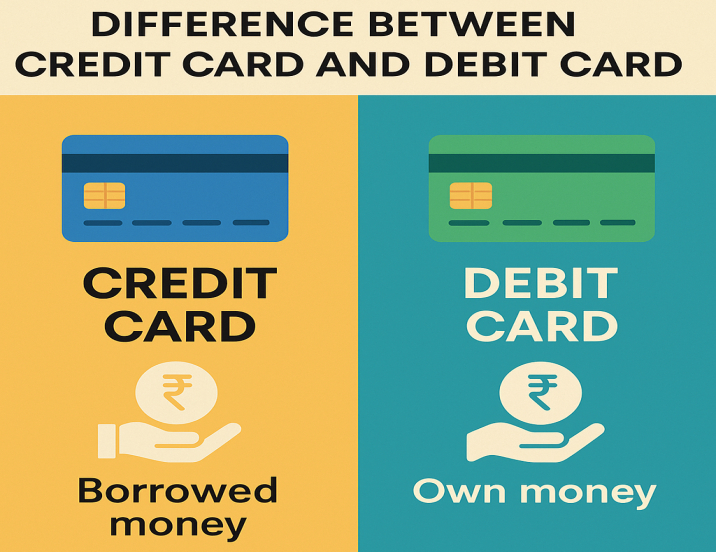

A debit card is connected to your bank account, and the money is taken directly from it whenever you make a payment. Whenever you pay or withdraw money using a debit card, the amount is immediately taken out from your bank account.

Key Features of Debit Cards:

- Directly connected to your savings or current account.

- You can only spend what you already have.

- Works for online and offline payments, ATM withdrawals.

- No interest charges.

Example: If you have ₹5,000 in your bank and make a ₹2,000 purchase, your remaining balance will be ₹3,000.

What is a Credit Card?

A credit card allows you to borrow money up to a certain credit limit to make purchases. You pay the borrowed amount back later, either in full or through monthly installments.

Key Features of Credit Cards:

- Not connected directly to your bank balance.

- You borrow money from the bank or financial institution.

- You get a monthly bill with a due date to repay.

- If you don’t pay the full credit card bill on time, the bank charges interest on the remaining amount.

Example: If your credit limit is ₹30,000 and you spend ₹5,000, you’ll get a bill to pay ₹5,000 (or minimum due) before the due date.

Key Differences Between Credit Card and Debit Card

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of Funds | Borrowed from the bank | Deducted from your bank account |

| Interest | Charged if not paid on time | No interest charges |

| Spending Limit | Based on credit limit | Based on available balance |

| Rewards/Cashback | Often better rewards | Limited or no rewards |

| Credit Score Impact | Affects credit score | No impact on credit score |

| Risk of Overspending | Higher | Lower |

Advantages and Disadvantages

Debit Card Advantages

- Helps in budgeting (you spend only what you have).

- No risk of debt or late fees.

- Ideal for everyday transactions.

Debit Card Disadvantages

- No credit score benefit.

- Limited rewards or offers.

- Less protection in case of fraud.

Credit Card Advantages

- Helps build a credit score.

- Attractive rewards, cashback, and EMI offers.

- Useful in emergencies and big purchases.

Credit Card Disadvantages

- Risk of falling into debt if not used wisely.

- Interest charges and late fees.

- May encourage overspending.

When Should You Use a Debit Card?

- You want to stay within your budget.

- You prefer direct spending without future bills.

- You want to avoid debt or interest charges.

When Should You Use a Credit Card?

- You want to build your credit history.

- You aim to pay the entire credit card bill every month to avoid interest.

- You want access to rewards, offers, and emergency funds.

Tips to Use Both Wisely

- Use debit cards for daily expenses and budgeting.

- Use credit cards for planned purchases and pay on time.

- Set alerts to avoid missed payments or overdrafts.

- Keep track of your expenses through apps or SMS alerts.

Conclusion

Both credit and debit cards offer convenience, but they serve different purposes. Debit cards are best for controlling spending and avoiding debt, while credit cards can help with rewards and credit building—if used responsibly.

Understanding the difference between credit and debit cards helps you make smarter financial choices. Whether you’re shopping online, managing monthly expenses, or building your financial profile, use each card type with a clear strategy.

Learn more about Finance

![]()