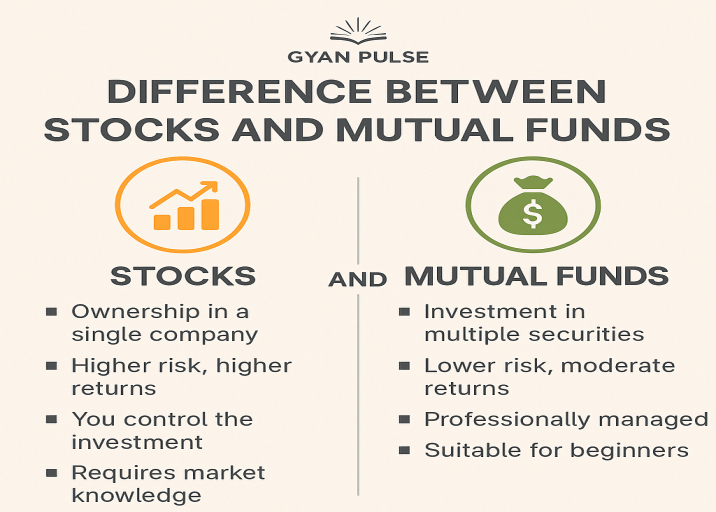

What is EMI? Meaning, How it works & How to calculate it easily, Full details 2025 Updated

What is EMI? Meaning, How it works & How to calculate it easily, Full details 2025 Updated.

What is EMI, Meaning – How it works and How to calculate it

In today’s world, loans have become a common financial tool, be it for buying a house, a car, or even funding education. One term you’ll often hear in this context is EMI. Whether you’re planning to take a loan or already have one, understanding what EMI means and how it works is crucial to managing your finances smartly.

Table of Contents

Let’s break it down in a simple and easy-to-understand way.

What is EMI?

EMI stands for Equated Monthly Installment. It is a fixed payment amount made by a borrower to a lender every month until the loan is fully paid off. Each EMI includes two components:

- Principal – the portion that goes toward repaying the actual loan amount.

- Interest – the portion that goes toward paying the interest charged by the lender.

So, every time you pay your EMI, a part of it reduces your loan balance (principal), and the rest is the cost of borrowing (interest).

How Does EMI Work?

When you take a loan, the lender calculates the total amount to be paid back over time, including interest. This total is then divided into equal monthly payments (EMIs) spread across the loan tenure.

In the initial months, a larger portion of the EMI goes toward interest, and a smaller portion toward the principal. As time goes on, the interest portion reduces and the principal portion increases. This is known as the reducing balance method, the most common EMI calculation method used by banks and financial institutions.

How to Calculate EMI?

The EMI can be calculated using a standard mathematical formula: EMI=P×R×(1+R)N(1+R)N−1\text{EMI} = \frac{P \times R \times (1 + R)^N}{(1 + R)^N – 1}EMI=(1+R)N−1P×R×(1+R)N

Where:

- P = Principal loan amount

- R = Monthly interest rate (annual rate divided by 12 × 100)

- N = Loan tenure in months

👉 Example:

If you take a loan of ₹5,00,000 at an annual interest rate of 10% for 5 years (60 months):

- P = 5,00,000

- R = 10 / 12 / 100 = 0.00833

- N = 60

Just enter the values into the EMI formula, and you’ll get your monthly payment amount. You can also use online EMI calculators available on bank websites or financial apps to make this process easier.

Types of EMIs

- Home Loan EMI – Usually of large value and longer tenure.

- Car Loan EMI – Medium-sized EMIs, usually for 3–5 years.

- Personal Loan EMI – Shorter term but higher interest.

- Education Loan EMI – Sometimes EMI payments often begin only after the course ends, this waiting time is called the moratorium period.

- Consumer Durable Loan EMI – For products like phones, TVs, and furniture, often with zero-interest offers.

Benefits of EMI

- Affordability: You don’t have to pay the full amount upfront.

- Predictability: You’ll know the exact amount you need to pay every month, no surprises.

- Flexibility: Many lenders offer custom EMI plans – step-up, step-down, or balloon EMIs.

- Improved Credit Score: Timely EMI payments help build a strong credit history.

Tips to Manage Your EMIs Smartly

- Borrow only what you can repay comfortably.

- Make sure your EMI doesn’t exceed 40% of your monthly income to stay financially comfortable.

- Pick a loan tenure that fits your budget – longer tenures mean smaller EMIs, but you’ll pay more interest overall.

- Avoid late payments, they can hurt your credit score and attract penalties.

- Prepay when possible, this helps reduce your interest burden.

Final Thoughts

Understanding EMI meaning and how it works is the first step toward becoming financially responsible. Whether you’re planning a big purchase or managing existing loans, having clarity on EMI can help you budget better and avoid financial stress.

Use an online EMI calculator before taking a loan, compare interest rates, and always read the fine print. Smart planning now can help you save big in the future.

Learn More about Finance

![]()